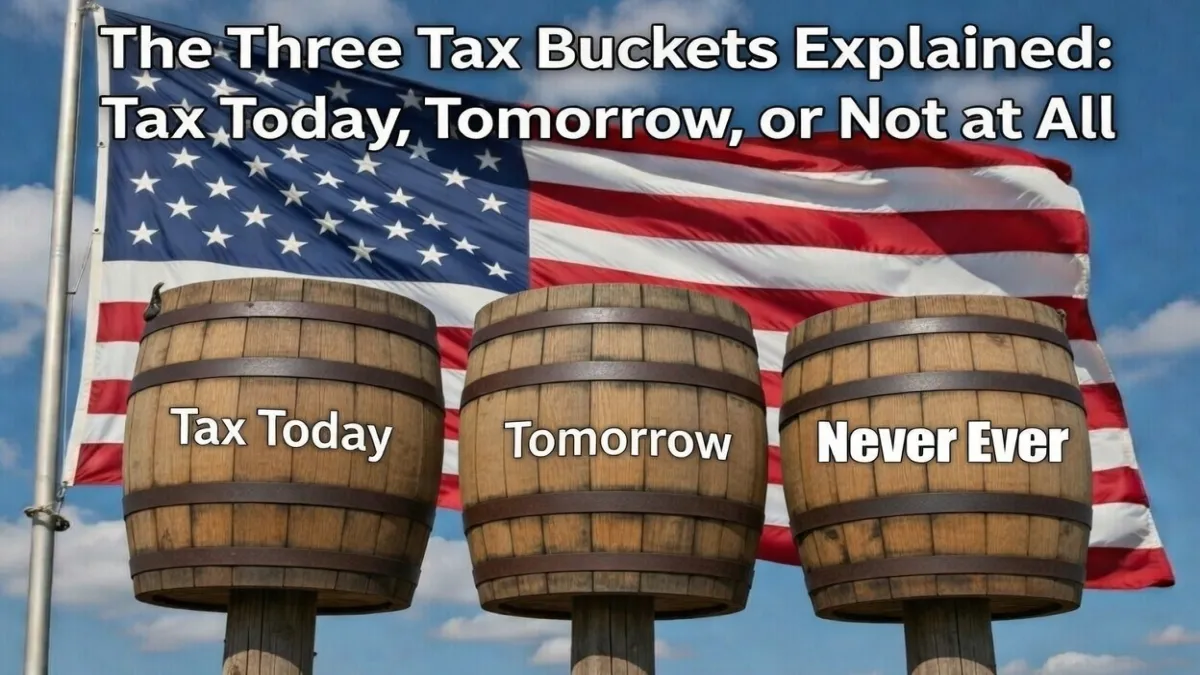

Three Tax Buckets: Taxes may be inevitable, but the timing of when they are paid on investments can differ significantly. Financial planners often describe this timing difference using a simple framework: three tax buckets — pay tax now, pay tax later, or potentially avoid tax on future growth. While the idea sounds straightforward, its implications for retirement income, long-term wealth creation, and financial flexibility are far-reaching.

The concept has gained attention among salaried employees, federal workers and private sector professionals who are trying to balance rising living costs with retirement preparedness. Based on available documents and financial planning discussions, the way investment growth is taxed can influence not only annual returns but also the amount of income available decades later. In practical terms, understanding these buckets helps investors decide how to diversify not just assets, but tax exposure as well.

Taxable Accounts and the ‘Pay Now’ Structure

The first category includes what planners call the “tax now” bucket. These are regular savings accounts, fixed deposits, brokerage accounts, bonds and mutual funds held outside retirement accounts. The principal invested typically comes from income that has already been taxed. However, any interest, dividends or capital gains generated during the year may also be taxed annually.

Investors usually receive tax forms summarising the growth, which must be reported as income. While this reduces compounding slightly because a portion goes toward taxes each year, these accounts offer liquidity and flexibility. For example, an investor saving for a house down payment may prefer a taxable account because funds can be accessed without retirement-related restrictions. The trade-off is that annual tax liability may apply depending on gains and prevailing rates.

Deferred Tax Accounts and Future Liability Considerations

The second bucket is commonly referred to as “tax later” or tax-deferred. Traditional retirement accounts such as a traditional IRA, 401(k), 403(b) or Thrift Savings Plan fall into this category. Contributions are generally made using pre-tax income, reducing current taxable earnings. This immediate relief can be beneficial for individuals in higher income brackets today.

However, withdrawals in retirement are typically treated as taxable income under prevailing rules. The assumption behind this strategy is that an individual may fall into a lower tax bracket after retiring. That may work in some cases, but this may vary by case depending on pension income, investment withdrawals and changes in tax policy. A financial advisor explains, “Deferral is not avoidance. Investors should project what their income might look like later rather than focusing only on today’s deduction.”

Tax-Free Growth Accounts and Long-Term Strategy

The third bucket, often described as “tax never” in terms of growth, includes accounts such as Roth IRAs, Roth 401(k)s and Roth versions of employer-sponsored savings plans. Contributions are made with after-tax income, meaning there is no upfront deduction. However, qualified withdrawals, including earnings, may be tax-free if conditions under IRS rules are met.

Other examples sometimes cited include education savings accounts, certain college plans and municipal bond income, though each has its own eligibility criteria. In practical terms, this structure can offer flexibility in retirement, especially when managing taxable income thresholds. For instance, withdrawing from a Roth account during a high-income year may help avoid pushing total income into a higher bracket. Verification is recommended before assuming tax-free treatment, as specific conditions must be satisfied.

Why Tax Diversification Matters in Retirement Income Planning

Relying heavily on just one bucket can limit choices later. If all savings sit in taxable and tax-deferred accounts, retirees may have limited control over their annual tax exposure. Required minimum distributions from traditional accounts, for example, may increase taxable income regardless of personal spending needs. According to reports, this can also influence Medicare premium calculations and other income-linked charges.

A diversified approach spreads funds across all three categories. Consider a retiree who needs $60,000 in annual income. If part of that comes from a Roth account and part from a taxable account, they may manage tax brackets more efficiently. In contrast, drawing the full amount from a tax-deferred account could increase overall liability. Results depend on individual circumstances, but flexibility often becomes a valuable asset in later years.

Evaluating the Right Mix: Individual Factors and Policy Changes

There is no universal formula for allocating money across the three tax buckets. Age, income level, expected pension benefits, estate planning goals and potential legislative changes all influence the decision. Younger workers in lower tax brackets might lean toward tax-free growth options, while mid-career professionals in higher brackets may value immediate deductions.

It is also worth noting that tax laws evolve. Past decades have seen revisions in contribution limits, withdrawal rules and income thresholds. As per guidelines, investors should review account statements, consult official IRS publications and consider speaking with a qualified financial planner before making adjustments. Policy updates could alter assumptions about future rates, making periodic reassessment essential.

Clarification on Growth Versus Principal

A common misunderstanding involves the difference between principal and earnings. In tax-free growth accounts, the initial contribution has already been taxed, but future gains may qualify for tax-free withdrawal if eligibility criteria are met. In tax-deferred accounts, both principal and growth are usually taxable upon withdrawal.

This distinction becomes important when calculating retirement income streams. For example, withdrawing $10,000 from a traditional account could increase taxable income for that year, while a similar withdrawal from a qualified Roth account may not. However, penalty may apply under rules if withdrawals occur before required holding periods or age thresholds. Reviewing official documentation ensures compliance and accurate planning.

Disclaimer

This article is intended for informational purposes only and is based on general financial planning concepts. Tax outcomes depend on individual circumstances and prevailing regulations. Readers are advised to consult official guidance or seek assistance from a qualified tax or financial professional before making investment or retirement planning decisions.